Many businesses pay attention to accounts payable only when an issue arises. A supplier follows up on an overdue invoice, a duplicate payment is identified, or month-end reporting takes longer than expected. More often than not, these situations point to gaps in the underlying process rather than isolated mistakes.

Accounts payable is more than an administrative responsibility. It determines when payments are made, who authorises them and how financial obligations are recorded and tracked. A well-structured AP function provides visibility over liabilities, reduces the risk of errors and fraud and helps maintain consistent supplier relationships.

Whether a business is refining an existing process or addressing recurring inefficiencies, a clear understanding of accounts payable can make a meaningful difference. The following sections discuss the key stages of AP, common pain points and approaches that improve accuracy and control.

Key takeaways

- The accounts payable process is only as reliable as the controls built into it, not just the steps followed.

- Three-way matching, segregation of duties and vendor master data governance prevent most AP fraud and duplicate payments.

- Delays in AP cost supplier credit terms, early payment discounts and cash flow visibility, not just processing time.

- Outsourcing accounts payable gives Australian businesses access to a structured AP function without building one internally.

What Does Accounts Payable Mean?

Accounts payable refers to the money a business owes to its suppliers or vendors for goods or services received but not yet paid for. In simple terms, what is accounts payable? It is the record of all unpaid bills and invoices that a company must settle within a specific period, usually within one year.

Importance in Accounting and Business Operations

Accounts payable in accounting is classified as a current liability on the balance sheet, representing short-term financial obligations that must be paid. Effective management of accounts payable helps businesses avoid late fees, maintain strong supplier relationships and ensure accurate financial reporting. It also supports healthy cash flow by tracking what the business owes and when payments are due.

A well-managed accounts payable process includes receiving and approving invoices, scheduling payments and maintaining payment histories. In larger organisations, this may be handled by a dedicated accounts payable department, while small businesses often manage it through bookkeepers or automated systems. Proper handling of accounts payable is essential for compliance, business planning and maintaining a positive credit reputation.

Additionally, accounts payable should be distinguished from accounts receivable, while accounts payable is money the business owes, accounts receivable is money owed to the business by customers. Both are crucial for cash flow management and accurate financial statements.

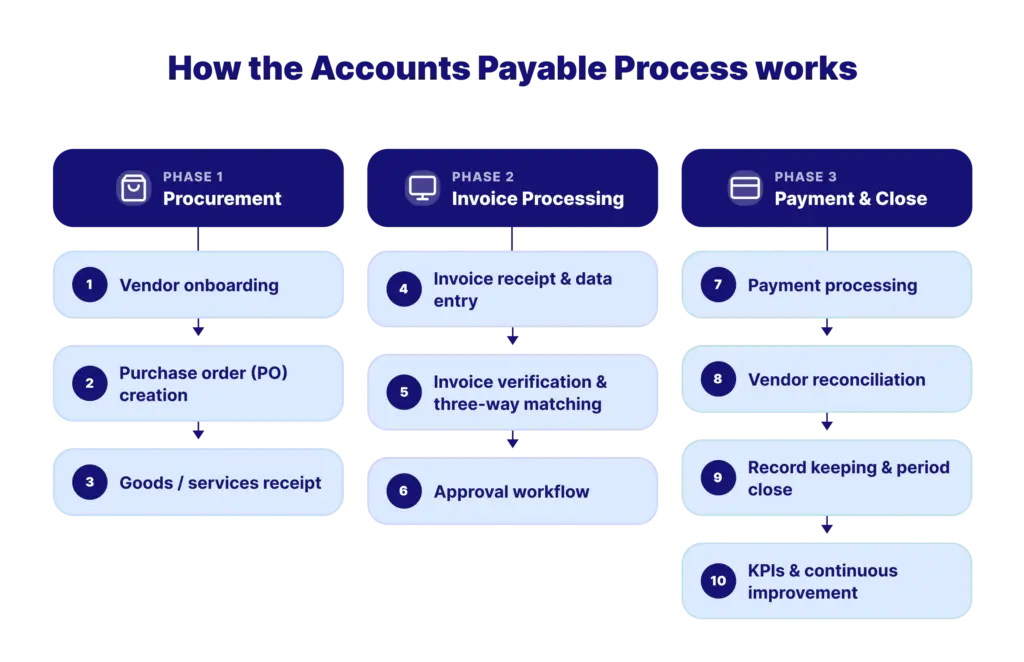

Accounts Payable Process: Step-by-Step

The accounts payable process follows a structured sequence, with each stage building on the one before it. From setting up a supplier to recording the final payment, every step plays a role in ensuring invoices are processed accurately, approved appropriately and supported by a complete audit trail. The flow below provides an overview of the full accounts payable cycle discussed in the following sections.

Each stage serves a specific purpose in maintaining accuracy, control and timely payments. The following sections explain every step in more detail.

Step 1: Vendor onboarding

Before any invoice can be paid, the supplier needs to be set up correctly, with legal details confirmed, bank account information verified and payment terms agreed. Most payment fraud begins at this stage, through unauthorised vendor creation or unverified changes to bank details. Restricting who can create or edit vendor records is the single most effective control here.

For example, a business onboards a new supplier without a formal verification step. Months later, someone requests a bank detail change. It looks legitimate. No one checks it directly with the supplier. The next payment run sends funds to an account the real supplier has never used.

Step 2: Purchase order creation

A purchase order documents what was agreed before delivery: quantity, price and terms, in writing. Without it, invoice verification has no baseline to check against.

For example, a business orders stock without raising a purchase order. When the supplier invoice charges for a different quantity, there is nothing documented to dispute it. The invoice gets paid because no record says it should not be.

Step 3: Goods and services receipt

When goods are delivered or services are completed, the receipt is recorded against the original purchase order. This record is what makes matching possible later.

For example, a business records full delivery on a partial shipment. The next invoice from that supplier creates a matching discrepancy, and payment is held up until someone traces the error back to the receipt record.

Step 4: Invoice receipt and data entry

Vendor name, invoice number, purchase order reference, line items, amounts and payment terms all need to be captured accurately, and checked against existing records to catch duplicates before the invoice enters the workflow. Many Australian businesses now use dedicated data entry services to keep this step accurate and fast, particularly once invoice volume grows past what one person can key by hand.

For example, a business receiving forty invoices a week by email and PDF finds two or three duplicate entries every month once volume passes a certain point. Structured capture at this step catches the duplicate before it reaches approval, rather than after payment.

Step 5: Invoice verification and three-way matching

Three-way matching compares the invoice against the purchase order and the goods receipt record. All three need to agree on quantity, price and delivery before an invoice moves to approval.

For example, a business receives an invoice for 500 units from a regular supplier. The goods receipt record shows 420 were delivered. Matching catches the discrepancy before the invoice reaches approval. The supplier is contacted, the correct amount is confirmed and payment goes out accordingly.

Knowing what to put on an invoice to get paid faster reduces matching errors and speeds up the entire cycle.

Step 6: AP approval workflow

Invoices that pass matching are routed to the relevant approver based on value and cost centre. Approval workflows built on email chains create delays and audit trails that are hard to reconstruct later. Defined authority levels and automatic escalation keep invoices moving even when one approver is away.

Step 7: Payment processing

Approved invoices are scheduled around due dates and early payment discounts. Payment runs are processed under dual control, so the person who approves a payment is never the same person who releases it.

For example, a fraudulent email made to look like it comes from a known supplier requests a bank detail update. The email address differs from the real one by a single character. If the update is made without a phone check against the number already on file, the next payment goes to a fraudulent account.

Step 8: Vendor reconciliation and dispute resolution

Vendor statements are compared against internal records regularly, so missing invoices or unapplied credits are caught before they become larger problems.

For example, a business skips vendor reconciliation for several months. A year-end review turns up thousands of dollars in supplier credits that were never applied. The credits were real and on the supplier’s own records the entire time.

Step 9: Record keeping and period close

Purchase orders, receipts, invoices, approvals and payment confirmations all form the audit trail and need to be archived on a defined retention schedule.

The importance of record keeping for businesses becomes obvious the first time an audit or a supplier dispute requires proof of what happened and when. At month-end, the AP sub-ledger is reconciled to the general ledger and bank statements, and any goods or services received but not yet invoiced are accrued.

Step 10: KPIs and continuous improvement

Tracking invoice processing time, first-pass match rate, days payable outstanding and discount capture consistently turns AP from a function managed reactively into one that improves deliberately over time.

| KPIs | What it Measures | Industry Benchmark |

|---|---|---|

| Invoice Processing Time | Days from receipt to payment | 5 to 10 days |

| First-Pass Match Rate | Invoices matched without exception | Above 85% |

| Days Payable Outstanding | Average days taken to pay invoices | 30 to 45 days |

| Early Payment Discount Capture | Available discounts taken | Above 90% |

| Duplicate Payment Rate | Invoices paid more than once | Below 0.1% |

| Cost Per Invoice | Total AP costs divided by volume | Compare against your own baseline |

Tracking these consistently turns AP from a function managed reactively into one that can be improved deliberately.

The Accounts Payable Framework: Controls that keep the process reliable

Having a process is not the same as having a framework. A process describes what happens. A framework defines who is authorised to do it, what controls are in place to prevent errors and fraud and how the business confirms those controls are working.

An accounts payable framework is the set of controls, approval structures and process standards that ensure vendor payments are accurate, authorised and fully traceable.

- Segregation of duties: The person who creates a vendor record should not approve invoices from that vendor or release payments to them. In smaller teams where one person handles several AP functions, management review of every payment run before release becomes the compensating control.

- Vendor master data governance: Access to create vendors or change bank details needs to be restricted to named people, logged and reviewed regularly.

- Three-way matching: For any business processing a meaningful volume of invoices, this is the baseline check against overbilling.

- Audit trail completeness: Every action, received, matched, approved, paid, needs a timestamp and a user record.

The process and the framework work together. One without the other leaves gaps that only become visible when something goes wrong.

Common Accounts Payable Challenges

Even a structured AP process runs into recurring friction points:

- Manual data entry errors. Manual capture increases duplicate payments, wrong coding and missed entries.

- Matching discrepancies. Mismatches between purchase orders, receipts and invoices delay approval and hold up payment.

- Slow approvals. Paper-based or email-driven approval chains cause missed due dates and lost discounts.

- Fraud exposure. Weak segregation of duties and unverified vendor changes are the two biggest entry points for AP fraud.

- Poor record keeping. Disorganised archives slow month-end close and complicate audits.

- Reconciliation gaps. Unreconciled vendor statements leave missing invoices and unapplied credits sitting unresolved for months.

None of these need a full rebuild to fix. Most come down to documented ownership, defined timeframes and consistent controls at each stage.

Is your AP Process actually working?

Running an AP process and running it well are two different things. The difference shows up not in whether payments are going out but in how accurately, how efficiently and with how much visibility.

Signs it is working:

- Invoices are processed and approved within agreed timeframes without manual follow-up

- Three-way matching exceptions are resolved quickly with a clear owner each time

- Month-end close is consistent and produces minimal late adjustments

- Supplier statements reconcile cleanly on a regular basis

- Early payment discounts are captured regularly

- The business can state its current AP liability position accurately at any point in the month

Signs it is not:

- Suppliers contact the team about invoices that have not been processed yet

- Duplicate payments appear during reconciliation

- Month-end regularly produces invoices not captured during the month

- Invoices wait because an approver is unavailable

- More time goes into entering and chasing data than reviewing and resolving it

When several of these signs appear together, the issue is rarely one person or one invoice. It is usually a process gap that has been present for some time and is now visible enough to cause problems.

AP Automation: What it changes and what it does not?

As invoice volumes grow, manual AP processes become harder to sustain. The time cost increases, the error rate rises and the team spends more time on routine work and less on decisions that require actual judgement.

AP automation removes manual effort from the parts of the process that follow predictable rules. Invoice capture, matching, approval routing, payment scheduling and reporting can all be handled automatically. What automation does not do is replace the judgement needed to resolve exceptions, verify vendor changes or make decisions about disputed invoices.

What automation handles well:

- Capturing invoice data from emails, portals and structured electronic formats

- Matching invoices against purchase orders and goods receipt records

- Routing invoices to the correct approver based on value and cost centre

- Identifying exceptions and potential duplicates for human review

- Scheduling and processing payment runs

- Updating records and producing reports without manual intervention

What still requires a person:

- Investigating exceptions that do not have a clear resolution

- Verifying changes to vendor bank details before payments are processed

- Reviewing transactions that fall outside normal patterns

- Making decisions on disputed invoices

- Maintaining vendor master data and keeping approval structures current

Automation is most effective when it handles volume and consistency and people focus on the work that requires judgement.

For businesses evaluating whether automation makes sense, the starting point is understanding which parts of the current process consume the most time and produce the most errors.

How Australian Businesses are managing their AP Function?

Australian businesses are generally taking one of three approaches to AP. The right one depends on invoice volume, internal resource and how much of the function the business wants to manage directly.

Managing AP internally

Building an AP function in-house means dedicated staff, accounting software configured for the business’s specific workflows and internal controls owned and maintained by the finance team.

Accounts payable works when invoice volumes justify the resource and when the business has the capacity to keep the process current as it grows.

Using AP features within existing accounting software

Choosing the right accounting software is often the starting point for businesses looking to improve their AP function.

Xero, MYOB and NetSuite all have AP functionality built in, including invoice capture, approval routing, payment scheduling and reporting.

Many Australian businesses already use one of these platforms but have not fully configured the AP features available to them.

Some businesses pair their bookkeeping software with a dedicated invoicing software tool for capture, which reduces manual entry without a full platform change.

Outsourcing accounts payable to a specialist provider

For businesses whose internal teams do not have capacity for AP, whose invoice volumes do not justify a dedicated resource, or whose current process is not keeping pace with growth, outsourcing accounts payable services is a structured alternative.

Accounts Payables outsourcing gives access to established processes and experienced people without the cost of building an AP team from scratch. The provider brings the people, the process and the technology. The business accesses a functional AP operation without building or managing it directly.

Some businesses outsource accounting services in full, folding AP into the same arrangement as outsource bookkeeping. Others outsource accounts payable on its own, alongside bookkeeping managed internally. Both are common, and the right setup depends on where the business already has capacity.

What Outsourcing Accounts Payable Services looks like in practice?

Outsourcing accounts payable does not mean losing control. The business retains authority over every approval and every vendor relationship decision. What changes is who manages the workflow between invoice receipt and the point where the business needs to act.

What outsourcing accounts payable services typically covers:

- Invoice receipt and capture: Invoices are received, digitised and entered into the workflow. Duplicates are identified before processing begins.

- Verification and matching: Three-way matching is performed on every invoice. Exceptions are assigned to a defined resolution process with a named owner and a clear timeframe.

- Approval coordination: Invoices requiring sign-off are routed to the right person. The provider manages the workflow. The business makes every approval decision.

- Payment preparation: Payment runs are prepared according to due dates and discount opportunities and presented to the business for authorisation before anything is processed. Dual control is maintained throughout.

- Reconciliation and reporting: Vendor statements are reconciled on schedule. AP reports are produced consistently. Month-end close is supported with records that are current and complete. What the business retains: approval authority, vendor relationship decisions and any judgements about disputed invoices or transactions that fall outside the normal process.

What the business retains throughout: approval authority, vendor relationship decisions and judgement calls on disputed invoices.

When comparing payable services providers, check for a named account manager, transparent pricing against actual volume and client references in a similar industry. Not every one of the payable outsourcing companies active in Australia works the same way, some run a fully managed service, others handle only the processing layer.

Outbooks offers flexible engagement models for both accountants and businesses, so support can scale to whatever the internal team already covers.

For Australian businesses that have grown beyond what a manual process can handle but are not ready to hire a dedicated AP team, outsourcing accounts payable services provides access to a structured, consistent AP function without the cost of building one internally.

Outsourcing accounts payable allows businesses to focus resources on core activities.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

A well-managed accounts payable process gives a business confidence that payments are going to the right place, at the right time, under proper authority and with a complete record of every decision made along the way.

For Australian businesses managing AP manually or with a process that has not kept pace with growth, the gap between what the function costs today and what it should cost is worth examining honestly.

Whether the answer is tightening internal controls, making fuller use of existing software or choosing to outsource accounts payable services to a provider that already has the structure in place, the first step is an honest assessment of where the current process is falling short.

Outbooks provides outsourcing accounts payable services to Australian businesses that need a structured, reliable AP function without building one from scratch. To find out how we can help, email info@outbooks.com.au or call 0451 320 102.

Frequently Asked Questions

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.