Small businesses often record healthy sales but still face pressure managing daily payments because accounts receivable remains unpaid for weeks or months. While invoices sit unpaid, expenses such as payroll, supplier payments and operational cost continue regardless of when customers pay.

Accounts receivable factoring solves this mismatch by converting unpaid invoices into immediate working capital, helping businesses improve cash flow without waiting 30-90 days for customer payments.

This guide explains:

- How factoring accounts receivable works in practice

- How accounts receivable factoring improves cash flow movement

- How factoring supports working capital

- How businesses use AR factoring for stable growth

What Is Factoring Accounts Receivable?

Factoring accounts receivable (also known as AR factoring or invoice factoring) is the process of selling outstanding invoices to a third-party financial provider called a factor at a discount, in exchange for immediate cash. The factor then collects the invoice directly from your customers.

This differs from a loan: you are not borrowing against your receivables, you are selling them outright. As a result, factoring does not add liabilities to your balance sheet, which helps maintain a healthier financial position.

How Accounts Receivable Affects Business Cash Flow?

Accounts receivable represents earned but uncollected revenue. A $10,000 AUD invoice unpaid for 60 days creates cash flow gap funds can’t cover wages, inventory or growth despite recorded sales.

Factoring accounts receivable improves cash flow (cash movement) while strengthening working capital (current assets minus liabilities) by turning slow receivables into usable funds. As accounts receivable grows, operational cash shrinks, forcing supplier delays or lost orders. The core problem is not profitability; it is the delay between earning revenue and collecting cash.

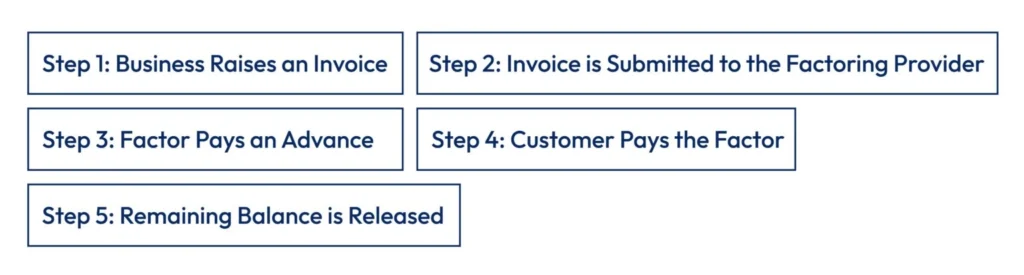

Step-by-Step Process of Factoring Accounts Receivable

Factoring accounts receivable follows a structured process that fits into normal billing systems.

- Step 1: Business Raises an Invoice: The customer receives an invoice with payment terms (e.g., 30 to 60 days).

- Step 2: Invoice is Submitted to the Factoring Provider: This is typically done through an online portal as part of the outsource accounts receivable management process.

- Step 3: Factor Pays an Advance: The provider pays an upfront amount (often a percentage of the invoice value). Types of factoring include factoring with recourse (business liable if customer defaults) vs non-recourse (factor takes risk, higher fees).

- Step 4: Customer Pays the Factor: Some arrangements are disclosed (customer pays the factor). Others may be confidential.

- Step 5: Remaining Balance is Released: Once payment is received, the remaining amount is paid to the business after fees.

Types of AR Factoring

Not all factoring arrangements work the same way. Understanding the main types helps you choose the right structure:

- Recourse factoring: If your customer doesn’t pay, you are required to buy the invoice back from the factor. Lower fees but you retain the credit risk. Most common in Australia.

- Non-recourse factoring: The factor absorbs the default risk if your customer doesn’t pay. Protects you from bad debts but fees are noticeably higher.

- Spot (selective) factoring: You choose individual invoices to factor on an as-needed basis. Useful when you need occasional funding rather than a continuous facility.

- Whole ledger factoring: You factor all or most invoices as standard practice. Better suited to businesses with high invoice volumes seeking consistent cash flow.

- Maturity factoring: The factor pays you on the invoice due date rather than upfront. Used mainly for credit protection rather than immediate liquidity.

Factoring Accounts Receivable Example

A simple invoice factoring example explains the financial impact:

| Item | Amount (in AUD) |

|---|---|

| Invoice Value | $10,000 |

| Advance (85%) | $8,500 |

| Customer Payment | $10,000 |

| Factoring Fee (2%) | $200 |

| Balance Released | $1,300 |

This factoring accounts receivable example shows how early funding improves cash availability and stabilises working capital.

Factoring Accounts Receivable Formula

A basic factoring accounts receivable formula explains the calculation:

Immediate Cash = Invoice Value × Advance Rate

Final Settlement = Invoice Value − Advance − Fees

These factoring accounts receivable formula highlights how receivables convert into cash through accounts receivable factoring.

How Factoring Improves Working Capital and Business Stability?

The main impact of accounts receivable factoring is seen in how working capital moves through the business.

1. Converts Receivables into Active Capital

Unpaid invoices are assets, but they cannot be used until collected. Factoring accounts receivable converts these assets into spendable funds, improving short-term liquidity.

2. Shortens the Cash Cycle

Without factoring, businesses may wait 60 to 90 days for payment. With accounts receivable factoring, this cycle is reduced to a few days. This strengthens factoring working capital management.

3. Improves Liquidity Without Borrowing

Since invoices are sold, not pledged, receivable financing factoring does not add liabilities. This helps maintain a healthy balance sheet.

4. Supports Sales Growth

With stable factoring cash flow, businesses can accept larger orders, invest in inventory and expand operations without waiting for payments.

5. Reduces Operational Stress

Reliable funding through factoring accounts receivable reduces payment delays, supplier issues and planning uncertainty.

Which Australian Industries Use AR Factoring Most?

Factoring is used across many sectors, but it’s especially common where payment terms are long and cash demands are immediate:

- Transport & logistics: Fuel, driver wages and maintenance costs arrive before freight invoices are paid.

- Construction & trades: Progress payments are slow but suppliers expect cash upfront.

- Manufacturing: Raw materials need funding before customers settle 60-day invoices.

- Staffing & recruitment: Weekly payroll with monthly client billing creates a permanent funding gap.

- Healthcare & NDIS providers: Insurance and NDIS reimbursements can take weeks to process.

- Wholesale & distribution: Thin margins mean any payment delay has an immediate operational impact.

Receivables Financing vs Factoring: Key Differences

While both options improve cash flow, they differ significantly in structure, control and disclosure, as outlined below.

| Aspect | Receivables Financing | Factoring |

|---|---|---|

| Ownership | Pledge as collateral | Sell outright (receivables purchase agreement vs factoring) |

| Collections | Business handles | Factor manages |

| Debt on balance sheet | Yes | No |

| Maturity Factoring | N/A | Pays on customer due date |

| Receivables Discounting vs Factoring | Loan-like, confidential | Often disclosed |

How Factoring Converts Receivables into Usable Funds?

AR factoring allows businesses to sell unpaid invoices to a financing provider in exchange for immediate cash.

This process is commonly known as AR factoring, factoring trade receivables or trade receivables factoring. The main purpose is to converts illiquid assets (unpaid invoices) into liquid working capital without creating debt on the balance sheet.

The mechanism differs from borrowing: instead of pledging receivables as collateral for a loan, businesses sell the invoice outright.

The factoring provider assumes collection responsibility, pays the advance immediately and releases the remaining balance (minus fees) once the customer pays.

This transforms the cash timeline from “wait 60 days” to “access funds in 2 days,” directly improving working capital availability.

Cost of Factoring Receivables and Cash Flow Impact

The cost of factoring receivables depends on several factors:

- Invoice volume

- Customer credit profile

- Dispute history

- Payment terms

- Service level

Typical factoring fees in Australia range from 1% to 5% of invoice value, with most standard 30-day arrangements sitting around 1.5–2.5% for businesses with creditworthy customers.

Fee structures vary, here’s what each means:

- Flat fee: a fixed percentage regardless of how quickly your customer pays. The simplest to budget for and most common in Australia.

- Tiered/split rate: starts lower and increases in blocks (e.g. every 10–15 days the invoice stays unpaid). Can become expensive if your customers pay late.

- What drives your rate higher: customers with poor payment history, small invoice volumes, long payment terms (60–90 days), high-dispute industries like construction.

- What drives your rate lower: creditworthy, consistently paying customers, high monthly invoice volumes, short payment terms (30 days).

Businesses should weigh the factoring fee against the real value of having cash two days rather than sixty days later for most, that trade-off is clearly worthwhile.

When Factoring Makes Sense & When It Doesn’t

It makes sense when:

- You’re waiting 45–90 days for payment while costs arrive weekly

- You’ve won a large contract but can’t fund it without cash now

- Your customers are creditworthy businesses but slow payers

- Collections are consuming staff time and resources

- You don’t qualify for a traditional bank line of credit

It may not make sense when:

- Your margins are very thin and factoring fees could push jobs into loss

- Your customers already pay reliably within 14–21 days

- Your customers would react badly to being contacted by a third party

- You operate in a high-dispute industry where invoices are frequently queried

- Your invoices relate to consumer transactions (most factoring is B2B only)

Role of Outsourced Accounts Receivable Services

Some providers combine factoring accounts receivable with outsourced accounts receivable services. These may include payment follow-ups, ledger maintenance, credit reviews and reporting.

For businesses facing collection delays, outsourced accounts receivable management strengthens internal controls alongside accounts receivable factoring.

Companies often compare models such as receivables financing vs factoring, receivables discounting vs factoring and receivables purchase agreement vs factoring before choosing the right structure.

Some arrangements also include factoring with recourse or maturity factoring depending on risk allocation.

Practical Considerations for Using Factoring

To gain maximum benefit from factoring accounts receivable, businesses should follow structured practices:

- Maintain accurate invoicing and documentation using most reliable invoicing softwares

- Monitor customer payment behaviour

- Review factoring fees regularly

- Avoid long-term over-dependence

- Integrate factoring into cash planning

These practices ensure accounts receivable factoring strengthens financial stability rather than masking internal weaknesses.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

Factoring accounts receivable improves cash flow by converting unpaid invoices into immediate funds. More importantly, accounts receivable factoring improves working capital by keeping money in circulation instead of locked in accounts receivable.

Through consistent factoring of accounts receivable, businesses stabilise liquidity, support growth and reduce financial uncertainty. Outbooks Australia offers outsourced accounts receivable services that pair seamlessly with factoring handling collections, ledger management and credit control to maximise your cash flow gains. Speak to our team today for tailored outsourcing acconting services.

Need support with managing your receivables and cash flow? Call us at 0451320102 or email info@outbooks.com.au to speak with our team today.

FAQs

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.