Keeping track of your transaction records in 2026 is more than just about following procedures; it provides clarity and control over your finances, allowing you to manage them much more smoothly. Whether you are a small business owner in Melbourne or managing your personal finances, clear and up-to-date records help you save time, spot issues and gain better insights into your expenses.

The need for proper transaction reconciliation and record-keeping is rising as businesses are switching over to digital tools and cloud based platforms which is an essential component of daily financial planning.

As proper record keeping becomes more important, staying organised is crucial for individuals. It ensures you don’t miss opportunities, overpay, or miss important deadlines.

If you do not keep proper records, you could face penalties and it might disrupt your long-term financial planning.

Let’s look at 10 benefits of recording transactions on time in the Australia.

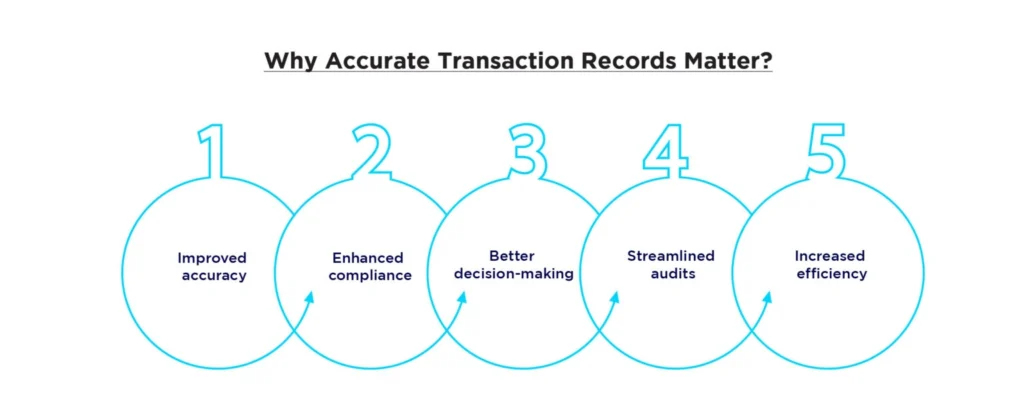

1. Helps you manage money

The main reason to send in transaction records on time is to know what’s happening with your money. Nobody wants unexpected cost, including your clients. When paying monthly bills, your record-keeping must match what you expect. With correct bookkeeping, you make sure everything is right. You avoid problems. It also gives you a clear picture of your profits and losses. You can then make better decisions about spending and investing.

2. Following government rules

The authorities are strict about following the proper procedures. You need to be careful when submitting reports and other documents. By recording every transaction daily, weekly, or monthly, you won’t have to worry about providing the right details. Submitting reports before deadlines ensures smooth operations. When you adhere to the set guidelines, you can run your business seamlessly and avoid unnecessary penalties, keeping your business in good standing.

3. Saves you money and time

Recording transactions on time helps you work more efficiently and boosts your return on investment. So, record every transaction and ensure you create an invoice for each one with the correct amount. Accurately record client payments to avoid errors or incorrect forecasts. This also helps you take full advantage of available benefits, saving you a lot of money over time.

According to a research from the Australian Bookkeepers Network businesses increased time efficiency by 30-40% who outsource bookkeeping services or use cloud based platforms like XERO.

4. Helps you make good financial choices

As a bookkeeper, you must provide accurate records to the decision-makers. This helps them make good choices for the future. It helps them stay competitive. Also, investors, shareholders and banks rely on these records. If you don’t give them the right data on time, why would they invest in your business? Accurate records allow businesses to make sound and strategic choices.

5. Spotting early red flags

Keeping good transaction records lets you see problems quickly. For example, you might spot late payments from customers. Or you might notice that your cost are rising. You can then take action to fix these problems before they become serious.

Want help identifying financial issues before they become costly? Contact Outbooks and let us handle your bookkeeping with precision.

6. Making your business more valuable

Good records make your business more valuable. If you ever want to sell your business, potential buyers will look at your financial records. If your records are clear and accurate, buyers will be more confident. This could help you sell your business for a higher price.

7. Improving relationships with suppliers and customers

When you pay suppliers on time, you build good relationships. They’ll be more likely to offer you good deals. And when you send customers accurate invoices, they’ll be more likely to pay you promptly. Good record-keeping helps improve relationships with everyone you work with.

8. Planning for the future

Good financial records are essential for planning. You can use them to create budgets and forecasts. This helps you see where your business is going. It also helps you make plans for growth and success.

9. Making better use of technology

By keeping your records up-to-date, you can make better use of accounting software and other tech tools. These tools can then provide valuable insights into your business performance.

10. Easier to get loans and investment

If you need to borrow money or attract investors, good financial records are vital. Lenders and investors want to see that your business is well-managed and financially sound. Clear and accurate records will increase your chances of getting the funding you need.

Keeping good records and sending them in on time might seem like a chore, but it’s really important. It helps you manage your money, follow the rules, save cash and make good choices. It also helps you spot problems, make your business more valuable and improve your relationships. By prioritising record-keeping, you’re setting your business up for a successful future. It’s a key part of running a healthy and thriving business.

These are the 10 benefits of transaction records Australia.

How Outbooks can help?

The significance of recording every transaction must not be degraded by a business. In the past few years, more and more accounting firms have started giving their tedious tasks to outsourced bookkeeping agencies. The team at Outbooks is glad to provide guidance with precise and proficient bookkeeping services for all accounting organisations.

Call us today at +61 861182913 or fill in our form to learn more about outsourcing accounting services.

FAQs

1. What does it mean by transaction record?

A comprehensive log of every financial activity your firm or you make such as sales, purchases, payments, invoices or receipts is known as transaction record.

2. Why is it crucial to lodge transaction records on time in Australia?

It helps ensure that your financial data is accurate and up to date, which helps avoid costly mistakes and keeps your business operations running smoothly.

3. How frequently should transaction records be updated?

Updating transaction records daily or weekly is the best choice to keep financial data manageable as waiting for too long results in mistakes and arises difficulty.

4. How does transaction reconciliation fit into record keeping?

The process of matching recorded transactions with bataxnk statements and invoices to ensure accuracy is transaction reconciliation. And doing it regularly helps spot errors early.

Get started with stress-free bookkeeping!

Let Outbooks help you save time and grow your business with expert bookkeeping support.

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.