Running a small or medium business in Australia means your bookkeeper carries real weight, accurate records, timely reconciliations, reports you can actually act on. When that breaks down, you rarely see it coming.

Bookkeeping mistakes rarely start with one big mistake. Usually, the signs are unreconciled accounts, misclassified transactions or delays in getting clear financial information.

Overtime, these problems affect the accuracy of your financial records and make it difficult to understand the true position of your business.

The ATO flags poor bookkeeping as a key driver of tax errors and ASIC consistently lists inadequate record-keeping among the leading causes of business failure. In 2023–24, more than 11,000 Australian companies entered external administration, many of them small businesses where financial visibility had already collapsed.

In this blog, we cover seven signs your bookkeeper may not be managing your books properly and why outsourcing bookkeeping services can help fix the issue early.

Key takeaways

- Reconciliations not completed monthly mean your financial reports cannot be trusted.

- Negative balances on a balance sheet or profit and loss statement almost always indicate a misclassification.

- A bookkeeper who never proactively flags issues is recording transactions, not managing your books.

- An opening balance equity account that is not zero is a sign of an incomplete setup and a ticking problem for your year-end.

- Loan balances that never change signal incorrect recording of principal and interest repayments.

- Outsourcing bookkeeping services give small businesses consistent reconciliations, accurate reporting and direct accountant coordination without relying on a single person.

Signs of a Bad Bookkeeper

A bad bookkeeper fails to reconcile accounts, misclassifies transactions (indicates as negative balance or a non-zero opening balance equity), does not update loan balances and never brings up any problems, basically making sure your accounting records are out of line with reality.

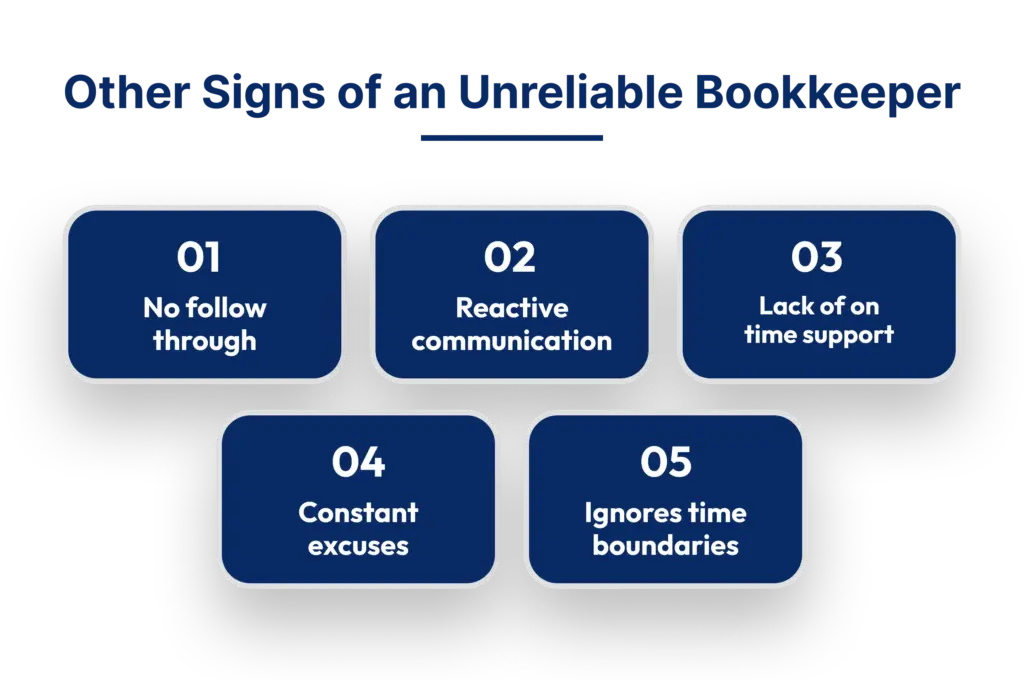

Sign 1: You are always the one following up

Your bookkeeper should be the one initiating contact sending monthly reports, flagging unusual figures and updating you without being asked. If your experience looks more like this:

- You send a message asking where last month’s report is

- You follow up two days later

- You receive partial information and have to ask again

That pattern is the problem. A bookkeeper who does not report proactively almost never reviews proactively either. The two go together. When no one checks your books unless prompted, errors build quietly in the background.

Sign 2: Bank and credit card reconciliations are not done monthly

Reconciliation is the process of matching every transaction in your accounting software against your actual bank and credit card statements. It confirms nothing is missing, duplicated or incorrectly recorded.

To check whether yours are being done, ask your bookkeeper to show you the reconciliation history for each account.

What you should see:

- A completed reconciliation for every month

- Covering every bank account and credit card

- With no unexplained gaps in the timeline

If the history shows months without a completed reconciliation, your financial reports are built on unverified data. Duplicated transactions, missing payments and incorrect entries remain unnoticed. Your profit and loss figures may look clean but reflect nothing close to what actually moved through your accounts.

Sign 3: Your balance sheet shows negative balances where there should not be any

Open your balance sheet and scan for negative numbers. Some are expected:

- Accumulated depreciation on equipment – normal

- A contra account your accountant set up intentionally – normal

What is not normal:

- A negative bank account balance (a bank would not allow a $333,000 overdraft, yet this appears in books more often than it should)

- A negative cost of goods sold figure on your profit and loss statement

- A negative loan or liability balance suggesting the bank owes your business money

These are not formatting issues. Each one represents a misclassification that changes your reported profit, distorts your financial position and creates extra work for your accountant at year-end. A bookkeeper actively reviewing your books catches these early. One who is only entering transactions does not.

Sign 4: The opening balance equity account is not zero

When accounting software is first set up and connected to your bank, it encounters existing balances it cannot automatically classify. It holds them temporarily in an account called opening balance equity. Your bookkeeper’s job is to identify what those balances represent and move them to the correct accounts. Once that is done, the opening balance equity account should read zero.

If it does not, it means those entries were never made. The unclassified figures are sitting in your equity balance, affecting your financial statements without being properly identified. Check your balance sheet for this account. Any amount other than zero is a sign of a setup that was never properly completed.

This is a particularly common issue when businesses switch accounting software or when a new bookkeeper takes over an existing set of books without properly reviewing the opening position.

Sign 5: Your loan balances never change

If your business has a loan and you have been making regular repayments, your loan balance on the balance sheet should decrease over time. Each repayment has two components:

- Principal – reduces the outstanding loan balance on the balance sheet

- Interest – recorded separately as an expense on the profit and loss statement

If your balance sheet shows the same loan balance at the end of this year as it did at the end of last year, either the repayments have not been recorded correctly, or the principal and interest have not been separated. Both are bookkeeping errors. Both affect how your financial position is read by your accountant.

This is also relevant for businesses using platforms like Xero or MYOB that have loan tracking features, the software will not correct the split automatically if it has been set up incorrectly from the start.

Sign 6: Your books do not match your year-end financial statements

At year-end, your accountant works from your books to prepare financial statements. If the figures in your accounting software do not match the statements your accountant produces, it means adjusting entries were made during the year-end process but never brought back into your records.

This creates two versions of your financial position:

- The one your accountant holds

- The one sitting in your software

They should be identical. If they are not, your records have a gap in them. In the event of any query or review of your financials, that mismatch becomes a serious problem and an entirely avoidable one. Your bookkeeper should be coordinating with your accountant at year-end to ensure adjusting entries are posted back into the software correctly.

The ATO requires businesses to maintain accurate financial records for at least five years. Discrepancies between your software and your lodged statements can expose you to unnecessary scrutiny.

Sign 7: Your bookkeeper has never once flagged anything unusual

A bookkeeper doing their job well does more than record what has already happened. They notice patterns. They raise concerns. When something unusual appears in your accounts, you should hear about it from them not from your accountant and not when it is already a problem.

If your bookkeeper has never:

- Flagged a supplier payment that looked unusual

- Noted a receivable that has been outstanding too long

- Questioned an expense that does not match prior periods

Then they are processing transactions, not managing your books. That distinction is the difference between keeping records and actively watching your financial position.

Given that ASIC data consistently shows poor financial oversight as a leading driver of business failure, this is not a minor difference, it is a structural one.

The right bookkeeper functions as a first line of financial awareness. They are not your accountant, but they should be close enough to your numbers to know when something looks wrong.

These are some other common signs your bookkeeper may not be providing the support you need.

What are your options when your Bookkeeper is not working?

When the signs above feel familiar, most business owners consider three paths:

1. Keep the current bookkeeper and hope it improves

This rarely works without a structural change. If the reconciliations are not happening now, they will not happen without accountability built into the process.

2. Hire a full-time in-house bookkeeper

This solves the availability issue but not the oversight one. One person managing your accounts between other responsibilities faces the same constraints as before and comes with employment costs, leave cover and no built-in review layer.

3. Outsource bookkeeping services to a specialist team

This is where the structure changes. Monthly reconciliations as a standard deliverable. Team-based review. Direct accountant coordination. Defined reporting timelines you do not have to chase.

Why Outsourcing Bookkeeping Services changes the structure?

With bookkeeping outsourcing, you are not replacing one person with another person, you are replacing a single point of dependency with a process that has accountability built in at every step.

Here is what that looks like in practice:

- Monthly reconciliations completed as a standard deliverable, not an afterthought

- A team reviewing the books rather than a single person working in isolation

- Direct coordination with your accountant built into the process, so year-end is not a scramble

- Defined reporting timelines you do not have to chase

- Scalable support, as your transaction volume grows, your bookkeeping support grows with it

- No leave cover gaps, no single point of failure

For Australian small and medium businesses, the cost of outsourcing bookkeeping services typically starts from as little as $50 per month, significantly less than the accumulated cost of correcting poorly maintained records at year-end, or the risk of an ATO compliance issue stemming from inaccurate financial records.

Outsourced teams bring valuable experience with Australian-specific regulatory requirements, ensuring that your business stays compliant without relying on a single individual to keep up with evolving legislation and tax obligations

Beyond bookkeeping, many businesses also find value in management accounts, accounts payable outsourcing and accounting outsourcing services that give a more complete picture of financial health, not just a record of what has happened.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

If you recognised some of these signs in your own business, it may be time to take a closer look at how your books are being managed. Problems like missed reconciliations, incorrect balances and poor communication rarely fix themselves and often become expensive to correct later.

Good bookkeeping should give you clear, reliable numbers and confidence that your records are accurate. For many Australian SMEs, outsourcing bookkeeping services can be a practical way to bring more consistency, accountability and financial clarity to the process.

If your current bookkeeping process is no longer giving you confidence, it may be worth reviewing what support your business needs. To discuss your bookkeeping requirements, contact the Outbooks team on 0451 320 102 or email us at info@outbooks.com.au.

Disclaimer: We do not file Single Touch Payroll (STP), Pay Superannuation, provide SMSF services, or offer advice on pay rates or legal requirements such as tax rates applicable to non-residents working in Australia.

FAQs

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.