As 30 June approaches, many Australian business owners discover that their books are further behind than expected. Transactions have not been recorded, accounts have not been reconciled and the numbers no longer provide a clear picture of how the business is performing.

The ABS recorded recorded 2,729,648 actively trading businesses in Australia as of June 2025, this is a challenge many SMEs encounter at some stage. In many cases, the issue is not poor financial management but a bookkeeping backlog that has built up over time and now requires attention.

The good news is that catch-up bookkeeping provides a practical way to bring records up to date. This guide covers how to identify the scale of a bookkeeping backlog, what type of problem it is, how to clear it, what it costs and what prevents it from building up again.

Key takeaways

- A bookkeeping backlog means past periods have unrecorded, unreconciled or incorrectly coded transactions

- The oldest unreconciled period should always be tackled first, because catch-up work needs a clear starting point

- Catch-up bookkeeping and bookkeeping cleanup are two different problems and many backlogs need both

- Backlogs become harder and more expensive to clear as more periods are left unresolved.

- Catch-up bookkeeping in Australia is quoted as a project price after reviewing the file

- Getting records current before 30 June improves reporting accuracy, financial visibility and business decision-making

What is a Bookkeeping Backlog?

A bookkeeping backlog is a pile-up of past financial transactions that haven’t been recorded, sorted, or matched with your bank statements.

When you’re busy running a business, managing clients and focusing on operations, daily paperwork often gets pushed to the side. Before you know it, weeks turn into months. If your accounting software (like Xero or MYOB) doesn’t show your actual financial position right now, or if you have a mountain of unreconciled receipts from previous months, you have a bookkeeping backlog.

Common signs of a Bookkeeping Backlog

Your bookkeeping may need attention if:

- Bank and credit card accounts are not fully reconciled.

- Supplier invoices are missing or not matched to payments.

- Customer invoices and accounts receivable records are not up to date.

- Payroll records do not match pay runs completed this financial year.

- Business expenses have not been categorised correctly.

- A reliable profit and loss report cannot be produced when needed.

If two or more of these signs apply, there may be a bookkeeping backlog that should be addressed before 30 June.

Once a backlog has been identified, the next step is understanding its size. The amount of work involved often determines whether the records can be updated internally or whether additional support is needed.

Need to catch up on overdue records? Outsource bookkeeping to Outbooks and stay on track for EOFY.

What stage is the Backlog at?

The scale of the backlog determines whether clearing it before 30 June is realistic or whether the volume and complexity require professional support.

| Problem type | Catch-up Bookkeeping | Bookkeeping Cleanup |

|---|---|---|

| The problem | Entries are missing entirely | Entries exist but coded incorrectly |

| The work | Record what was never entered | Correct what was entered wrongly |

| The goal | Bring records to the present | Improve accuracy of existing records |

| When it applies | Books are behind | Books are current but unreliable |

A business that has been three months behind will often have both problems present. Missing periods are filled in first. Then existing records from those periods are reviewed for coding errors that accumulated while the books were not being maintained.

After identifying whether the backlog requires catch-up work, cleanup work, or both, the focus shifts to restoring the records in the correct order. The process should always begin with the earliest incomplete period and move forward from there.

How to fix a Bookkeeping Backlog?

When the books are behind, the instinct is often to start with the most recent period because it feels more manageable. This is the most common mistake in catch-up work. A recent period reconciled before earlier ones are verified carries every unresolved error from those periods forward.

The process works in one direction only oldest period first, then forward.

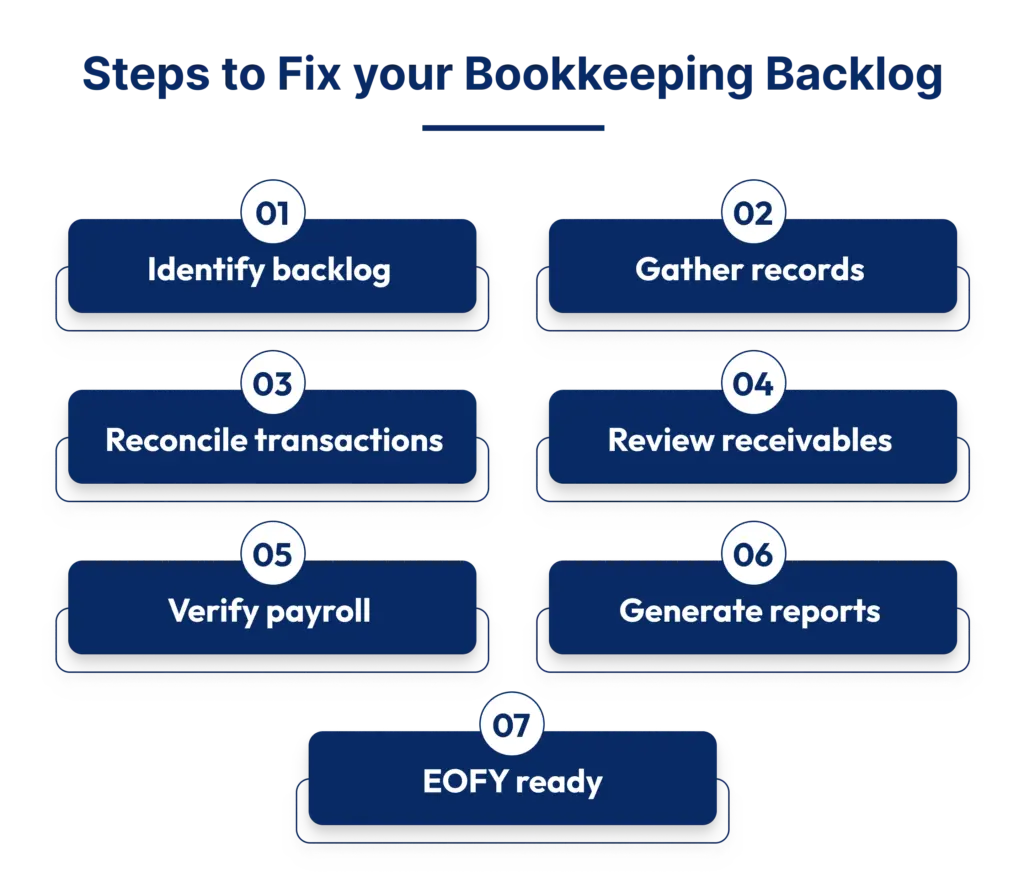

Step 1: Establish where the records stopped

Open the bank reconciliation report in the accounting software and find the earliest month with unreconciled transactions. That date is the starting point. Do not estimate it check directly. Knowing the full scope before beginning prevents discovering new gaps midway through.

Step 2: Gather every source document first

Collect the following for every period in the backlog before starting:

- Bank and credit card statements

- Supplier invoices and purchase records

- Customer invoices and sales records

- Payroll records for every pay run

Starting without complete documents means stopping mid-period each time something is missing, which breaks the sequence and creates errors in the entries being built.

Step 3: Reconcile period by period, moving forward

Each accounting platform shows unreconciled items differently:

- In Xero bookkeeping, unreconciled transactions appear as uncoded items in the bank feed waiting to be matched to an invoice, bill or ledger entry

- In MYOB bookkeeping, unmatched transactions sit in the bank reconciliation screen until reviewed and confirmed

- In QuickBooks bookkeeping, downloaded transactions remain in the Banking tab until categorised and accepted

The approach is the same across all three. Match every transaction to its source document, code it correctly and verify the period is complete before moving to the next one.

Step 4: Review accounts receivable and payable within each period

Before closing a period, confirm that invoices showing as unpaid are genuinely unpaid and that supplier bills are recorded for that period.

An invoice that was already received but never matched in the system inflates the receivables figure and flows into every report produced after it.

Step 5: Verify payroll records separately

Bank reconciliation reaching the current period does not resolve payroll. Each pay run needs to be matched against ledger entries gross pay, deductions and super obligations for every period in the backlog.

A payroll error found here must be corrected within the process. Leaving it means it compounds into every period that follows.

Step 6: Generate reports once every period is complete

Once every period is reconciled and payroll is verified, a profit and loss and balance sheet reflect the actual position of the business.

Not every business reaches this point immediately. In many cases, the backlog remains unresolved for longer than intended, which can create challenges beyond bookkeeping itself.

Risks of leaving a Bookkeeping Backlog unresolved

The consequences of an unresolved backlog are not just administrative. They show up in decisions, cash visibility and business cost.

- Cash figures become less reliable: Unmatched invoices and unreconciled accounts can create a misleading picture of available cash.

- Errors become harder to correct: Issues in payroll, expenses or transaction coding often spread across multiple reporting periods when left unaddressed.

- Finance applications face delays: Lenders typically require up-to-date financial statements. Incomplete records can slow approval processes.

- Business decisions carry greater risk: Hiring, pricing and investment decisions are only as reliable as the financial information behind them.

Poor record-keeping is a primary cause of errors at EOFY. ASIC lists inadequate financial records among the leading causes of business failure in Australia.

The impact of a backlog is not only about past records, it also affects how quickly the business can understand its current position.

How long does Catch-Up Bookkeeping take?

Three factors determine the timeline: how many periods are behind, whether payroll records are also incomplete and the condition of the source documents.

The actual timeline for any specific backlog is only clear after the file has been reviewed and the full scope established.

Catch-up bookkeeping or bookkeeping outsourcing often involves reviewing transactions, reconciling accounts, resolving discrepancies and verifying supporting records across multiple periods.

The amount of investigation required varies from one backlog to another, which can significantly affect the time needed to complete the work.

Time is only one side of catch-up bookkeeping. The other important factor is cost, which also depends on how much work is involved.

What does Catch-Up Bookkeeping Cost?

Catch-up bookkeeping is quoted as a fixed project price after reviewing the file, because the scope varies too much between backlogs for a standard rate to apply before the work has been assessed.

The factors that influence the cost are the same ones that affect the timeline:

- Number of periods behind

- Whether payroll records are also incomplete

- Condition and availability of source documents

A backlog with complete organised records costs significantly less to clear than one where documents need to be sourced or reconstructed before reconciliation can begin.

For reference, typical outsourcing bookkeeping hourly rates in Australia range from $50 to $120, with catch-up work at the higher end due to the investigation required per period.

Benefits of getting your Books up-to-date

Clearing the backlog is not just about avoiding problems. It changes what becomes available to the business.

- Cash flow becomes clearer: Financial records reflect current business activity, making spending and planning decisions more reliable.

- Business performance becomes easier to assess: Current reports provide a more accurate view of revenue, cost and profitability.

- More time for business priorities: Less time is spent locating records, correcting errors and answering bookkeeping queries.

- Finance applications can move forward: Lenders typically require up-to-date financial information before assessing an application.

Getting things back on track helps, but the real difference is made in how things are maintained after that.

Five practical strategies to prevent future Bookkeeping Backlogs

Getting the records current solves the immediate problem. These practices are what keep them current year-round.

- Reconcile accounts weekly: Regular reconciliations help identify discrepancies before they affect reporting and cash visibility.

- Follow a month-end close process: Reviewing accounts, payroll and financial reports each month helps maintain accurate records.

- Maintain supporting documents: Store invoices, receipts and other records consistently to avoid delays during reconciliations.

- Review receivables and payables regularly: Frequent reviews help identify outstanding items and maintain an accurate view of cash flow.

- Address process gaps early: Repeated delays in reconciliation, payroll or document management often indicate underlying process issues that require attention.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

A bookkeeping backlog rarely improves with time. The longer incomplete records remain unresolved, the greater the impact on reporting, cash flow visibility and EOFY preparation.

The first step is establishing the scope of the backlog. Once that is clear, the work can be prioritised and completed methodically, providing the accurate financial information needed for reporting and business decisions.

With 30 June approaching, reviewing your records early can reduce pressure and minimise disruptions during EOFY. If you need support to clear a backlog or maintain accurate financial records year-round, outsource bookkeeping to Outbooks and let our experienced team help keep your business EOFY-ready. Contact us on 0451 320 102 or info@outbooks.com.au

FAQs

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.