Construction businesses fail not because they run out of work but because they run out of money while the work is still happening. ASIC’s March 2026 data shows construction had more company failures than any other industry in Australia 24% of all business failures in the first eight months of 2025–26.

Small and medium construction businesses, including plumbers, electricians, builders, concreters and specialist subcontractors collectively known as trade SMEs, often find themselves in this position.

Bookkeeping for construction is structurally different from bookkeeping for any other small business. Each project has its own revenue, its own cost and its own margin. When the books do not reflect this, there is no real financial clarity at the project level or at the business level.

Here is what trade SMEs consistently get wrong when managing their construction bookkeeping and what a more accurate system looks like in practice.

Key takeaways

- Each construction project needs its own cost and revenue tracking. When everything is recorded together, there is no way to identify which jobs are generating profit and which are not.

- A high account balance during an active project period can be misleading if payments owed to vendors and subcontractors have not yet gone out.

- Variation orders and late subcontractor invoices, when not recorded in the correct period, produce job cost reports that do not reflect reality.

- Client retention must be recorded as a separate receivable against each project from the point it is first withheld, not grouped with general outstanding invoices.

- Equipment and plant cost absorbed into general overheads rather than individual jobs makes it impossible to calculate true project profitability.

- Cash payments made on site that are not documented the same day create gaps in the accounts that are difficult to trace and correct later.

Where Construction Bookkeeping often goes wrong?

Construction bookkeeping has layers that standard bookkeeping does not. Project-based billing, subcontractor management, equipment tracking and progress-based payments all create points where the books can go wrong. The following mistakes appear consistently across trade SMEs, regardless of business size or years of operation.

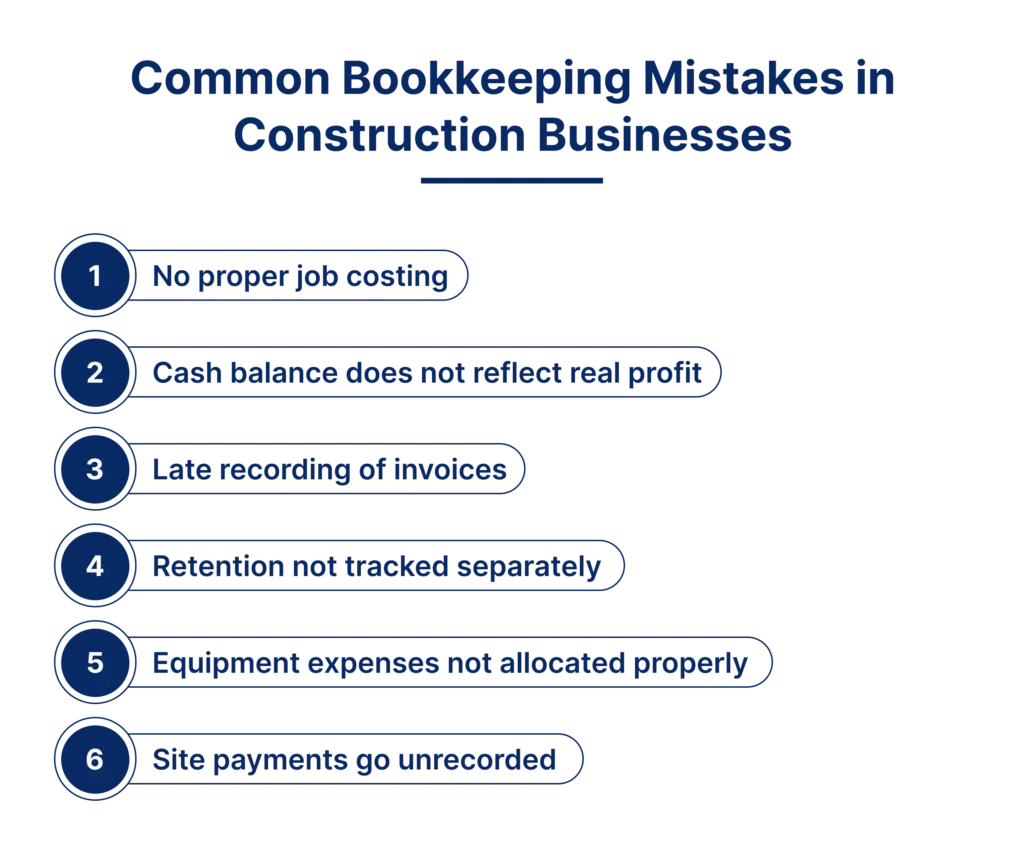

1. No proper job-costing

A trade SME running multiple projects at once is managing multiple separate financial units. Each job has its own labour, materials, subcontractors and agreed price.

Without tracking costs by project, there is no clear way to know which jobs are profitable until the work is already complete.

Job costing assigns every expense to the project it belongs to, using cost codes for labour, materials, subcontractors and equipment. This gives the business a clear budget-versus-actual view throughout the project, not just at the end.

| Without proper job costing | With proper job costing |

|---|---|

| Costs recorded together | Costs assigned to individual projects |

| Profit checked after project completion | Profit tracked throughout the job |

| Estimates based on assumptions | Quotes based on actual project data |

Without this visibility, future estimates are often built on incomplete information. A loss on one project can easily be repeated on the next, causing profit margins to decline over time.

2. Cash balance does not show real profit

A construction business with several active projects can show a healthy bank balance and still face cash shortage within weeks. Project expenses accumulate steadily but client payments come in at agreed stages.

Labour is paid weekly, supplier invoices fall due on fixed terms, and subcontractor payments need to be made regularly. This means a large part of the cash in the account may already be allocated to upcoming payments, leaving less available than the balance shows.

Without a clear schedule that matches expected income with future payments, cash shortages can happen unexpectedly. In many cases, the issue is not a lack of work, but a gap between when payments are received and when expenses need to be paid.

3. Late recording of invoices

Clients request additional work mid-project, materials get swapped and site conditions sometimes require work outside the original scope. Each change affects both the cost of the job and what the client owes. When these are not entered promptly, the job cost report stops reflecting reality.

A common example is additional work agreed verbally on site. The cost comes through via supplier invoices and labour but the extra amount the client agreed to pay never gets recorded. The job looks like it is running at a loss when it is not.

Subcontractor invoices can cause similar problems. If work completed in one month is recorded only when the invoice is received later, monthly figures become inaccurate and project performance becomes harder to assess.

4. Retention not tracked separately

Retention is often overlooked in bookkeeping for construction companies, even though it can add up to a significant amount over the life of a project.

In many Australian construction contracts, clients withhold a percentage of each progress payment until the work is complete and any defects have been resolved. When that amount is grouped with general receivables, it can easily be forgotten once the project ends.

| When retention is not tracked | When retention is tracked properly |

|---|---|

| It gets mixed into general receivables | It is recorded separately |

| Release dates are missed | Collection dates stay visible |

| Follow-up happens late | Recovery is reviewed regularly |

Tracking retention separately helps ensure earned revenue does not remain uncollected simply because it was not visible.

5. Equipment expenses not allocated properly

Plant hire, machinery, site vehicles and specialist tools often make up a large part of project spending. In many trade SMEs, these are recorded as general overhead instead of being assigned to the jobs that used them.

When equipment use is not included in the job report, projects can appear more profitable than they are. Future quotes are then based on incomplete figures, which can slowly reduce margins.

Hired equipment should be linked to the relevant project, while owned plant should be charged using an internal rate based on depreciation, servicing and insurance. This keeps job reports accurate and improves pricing decisions.

6. Site payments go unrecorded

Construction often involves payments made outside normal office processes. A site supervisor may buy materials on a personal card, a subcontractor may be paid before an invoice is raised or a day labourer may be paid at the end of a shift.

If these payments are not recorded at the time, they can be difficult to trace later. Missing receipts, unclear payment notes or no job reference can leave gaps in job reports and make account reconciliation harder.

A simple record at the time of payment, such as a receipt photo or a note against the job, helps keep project records complete and accurate.

Should you manage Construction Bookkeeping In-House or Outsource it?

Many trade SMEs decide how to handle bookkeeping when the business is still small and keep that arrangement in place long after the work volume and complexity has grown. It is a decision worth examining properly because the demands of construction bookkeeping are specific and the consequences of getting it wrong are significant.

Managing it in-house

In-house construction bookkeeping can work but it requires a skill set that goes beyond general bookkeeping. The person managing the books needs to understand:

- Job costing and cost code setup for construction projects

- Retention recorded as a separate receivable per project

- Subcontractor cost accrued to the correct reporting period

- Cash flow forecasting for progress-based payment structures

Without this, the accounts may look tidy but will not produce the job-level information the business needs to make sound decisions.

Outsourcing to a specialist

When construction bookkeeping is handled by a team that works specifically with construction businesses, the system is set up correctly from the start. This covers both bookkeeping and accounting for construction businesses, including job costing, reporting and financial oversight through outsourcing construction bookkeeping services not just basic transaction recording.

Job costing, retention tracking, subcontractor accruals and cash flow reporting are already part of the construction accounting outsourcing service.

A general bookkeeper will manage transactions accurately but will not flag that a retention amount has gone uncollected for months, or that a cash gap is developing in the coming weeks, or that subcontractor cost has been landing in the wrong period across multiple jobs. These observations require construction-specific knowledge.

Why Outsourcing makes more sense for most Trade SMEs?

For many trade SMEs, hiring a full-time bookkeeping specialist is not practical. Construction bookkeeping and accounting for trade SMEs goes beyond basic record keeping and includes job-level reporting, subcontractor tracking, retention monitoring and cash flow planning across projects.

This model gives access to expertise without the cost of a permanent hire. It also brings structure to project financials, so records reflect what is happening on site, not just what is entered in the system.

How it works for construction businesses?

The provider works on shared accounting and bookkeeping software, updates job records on a set schedule and flags issues early.

Missing subcontractor invoices, retention amounts approaching release dates and developing cash gaps are picked up before they affect reporting or cash flow.

What to look for?

Pick a provider that works specifically with construction businesses. Ask how they handle retention tracking, what their reporting schedule looks like and how they manage subcontractor accruals.

A general bookkeeper records transactions accurately. A construction specialist makes sure those records produce job-level information the business can actually use.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

Getting bookkeeping right in construction is not about keeping tidy records. It is about having accurate, job-level financial information the business can use to price work correctly, manage cash between payments and collect every amount owed including retention.

The mistakes in this blog are not rare. They appear across trade SMEs of every size and at every stage of growth. Whether they are caught early or not usually comes down to whether the right system is in place from the start.

Outsourcing bookkeeping for construction businesses should go beyond basic transaction recording. The right support should provide accurate job-level reporting, clearer project cost visibility and reliable financial data to help trade SMEs make better operational decisions.

Get in touch with the Outbooks team today to learn how a specialist bookkeeper for construction industry can support your business. Call us at 0451 320 102 or email us at info@outbooks.com.au for more details.

Frequently Asked Questions

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.