Struggling to track your business cash flow accurately or match expenses with the income they generate? Many small business owners face confusion choosing between accrual accounting vs cash accounting methods, which directly affects financial reporting accuracy and decision-making.

These two accounting basis approaches, cash basis accounting (recording transactions only when money changes hands) and accrual basis accounting (recognising revenue and expenses when earned or incurred), impact your profit picture, compliance and growth planning.

The right choice hinges on your business size, structure, financial complexity and turnover thresholds like Australia’s $10 million limit for cash basis eligibility in 2025.

With ATO guidelines emphasising proper accounting methods for GST and reporting, understanding accrual vs cash accounting differences is essential for small businesses, sole traders and growing enterprises to ensure accurate financial insights and regulatory compliance.

For Australian businesses, the ATO recognises both cash and accrual as valid accounting methods. Businesses with aggregated turnover under $10 million can choose either method. Those above $10 million must use accrual (non-cash) accounting for GST reporting.

In this guide, we’ll discuss:

- What cash accounting is and how it works

- What accrual accounting is and how it works

- Key differences between the two methods with real-life examples

- Advantages, disadvantages and compliance requirements

- Guidance on which method suits different business types

What is Cash Accounting?

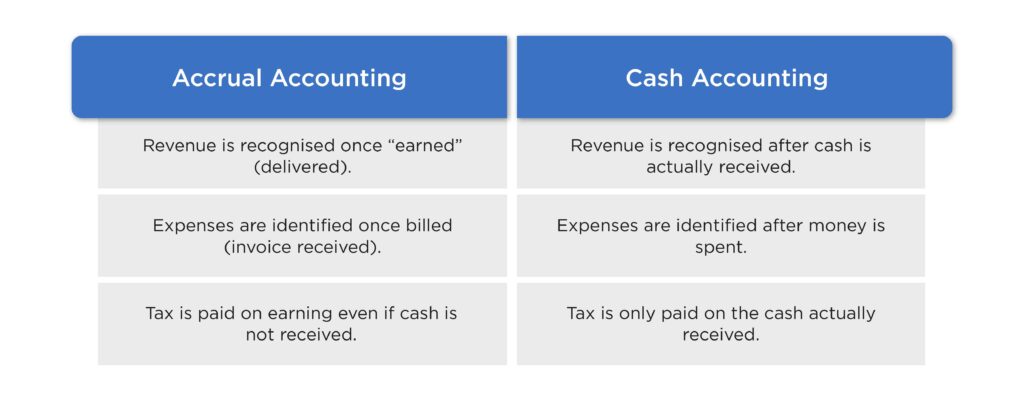

Cash accounting is a method where businesses record income only when payment is received and expenses only when bills are paid.

Also known as cash-basis accounting, it is popular among small businesses for its simplicity and ease of use. Only actual cash transactions are recorded, there is no tracking of unpaid invoices or bills, making it easy to monitor cash flow and manage day-to-day finances.

Cash accounting is best for businesses with simple transaction structures and those seeking straightforward financial management.

How Cash Accounting method works?

The cash accounting method follows these principles:

- Record income when cash is received

- Record expenses when payments are made

- No tracking of unpaid invoices or bills

- Focus on actual cash flow

What is cash accounting in practice? Imagine selling $1,000 worth of services in March. You only record this income when the customer pays in April.

Similarly, if you buy equipment in December but pay in January, you record the expense in January’s accounts.

Cash accounting provides a clear view of actual cash flow, making it simpler for small businesses to manage their finances. However, it may not provide a full picture of financial health since it excludes outstanding receivables and payables.

What is Accrual Accounting?

Accrual accounting records transactions when they occur, regardless of payment timing. This provides a complete financial picture.

The accrual accounting method matches income with related expenses in the same period. This gives better insight into business performance.

What is accrual accounting exactly? It recognises economic events as they happen, not when cash moves.

What is accrual accounting in practice?

Imagine completing a $1,000 project in March but receiving payment in April. Accrual accounting records the income in March’s accounts, reflecting when the work was done, not when payment arrived.

Similarly, if you incur an expense in December but pay in January, the expense is recorded in December.

Accrual accounting provides a more accurate view of financial health, especially for businesses with credit sales or purchases, by tracking all financial obligations and resources. It is commonly used by larger businesses and those required to comply with accounting standards.

How the Accruals basis of Accounting functions

The accruals basis of accounting operates on these principles:

- Income recorded when earned

- Expenses recorded when incurred

- Tracks outstanding invoices and unpaid bills

- Matches revenues with related costs

Using our previous example, a $1,000 March sale appears in March accounts. Payment timing doesn’t affect when it’s recorded.

Accrual accounting provides a more accurate view of financial health, especially for businesses with credit sales or purchases, by tracking all financial obligations and resources. It is commonly used by larger businesses and those required to comply with accounting standards, particularly those with an annual turnover above $10 million.

Key differences between Cash vs Accrual Accounting

The following table summarizes the main distinctions between cash and accrual accounting methods across key accounting aspects.

| Aspect | Cash Accounting | Accrual Accounting |

|---|---|---|

| Income Recognition | When payment received | When service provided |

| Expense Recording | When bill paid | When cost incurred |

| Financial Picture | Current cash position | Complete business performance |

| Complexity | Simple to manage | More detailed tracking |

| Suitable For | Small businesses | Growing/larger businesses |

Accrual Accounting Example

ABC Consulting completes a $5,000 project in December 2025. The client pays in February 2026.

Accrual accounting records:

- December 2025: $5,000 income

- Associated project costs in December

- Outstanding receivable until payment

Cash Accounting Example

The same ABC Consulting transaction under cash accounting:

- December 2025: No income recorded

- February 2026: $5,000 income recorded

- Expenses recorded when actually paid

This shows how accrual accounting provides a more accurate view of when income is earned and expenses are incurred, helping businesses better match revenues and costs in the correct period. In contrast, cash accounting focuses on actual cash flow timing, which may delay income and expense recognition but simplifies bookkeeping.

Who Should Use Each Method?

Cash or Accrual Accounting for Small Businesses

There is no single default method in Australia, the right choice depends on your turnover and business type. Most sole traders and small partnerships benefit from cash accounting due to its simplicity, but it is a choice, not a default.

Cash or accrual accounting choice depends on:

- Annual turnover levels

- Business complexity

- Future growth plans

- Investor requirements

When Cash Basis is Suitable

Cash basis works well for:

- Sole traders and small partnerships

- Service-based businesses

- Simple transaction structures

- Businesses wanting straightforward bookkeeping

Note: Eligible small businesses can use the cash basis method if their aggregated annual turnover is below $10 million. This threshold applies to both GST and general accounting purposes in Australia for 2025.

When Accrual Basis is Required

Accrual accounting is mandatory for businesses with aggregated turnover above $10 million, except that

eligible businesses may still use cash basis for GST (BAS) reporting purposes.

Required for:

- Limited companies

- Businesses over certain turnover thresholds

- Those seeking investment

- Complex business structures

Note: Businesses with an annual turnover above $10 million must use accrual accounting for GST and financial reporting. This requirement ensures compliance with Australian accounting standards and supports better financial transparency.

Choosing between cash and accrual accounting should consider current business size, complexity and future growth plans to ensure proper financial management and compliance with regulations.

Australia Legal Requirements and Changes

Cash Basis Rules: 2025–26 Update

For Australian businesses, there is no single “default” method, you choose based on your turnover and business type.

Key eligibility rules:

- Aggregated turnover under $10 million → can use cash or accrual

- Not carrying on a business but GST turnover is $2 million or less → can use cash basis

- Aggregated turnover above $10 million → must use non-cash (accrual) method for GST

- You can use different methods for GST and income tax, they do not need to match

Cash accounting considerations

A business can use cash accounting if it is registered for certain sales-based charges and its estimated turnover is $10 million or less.

Businesses with aggregated turnover above $10 million must use the accrual (non-cash) method for GST. The $2 million threshold applies separately, it covers entities not carrying on a business, who can still use cash basis if their GST turnover does not exceed $2 million.

Cash accounting for these charges on sales works differently from the approach used for income reporting. A business can choose different methods for each.

Many businesses use a hybrid approach in practice, cash basis for ATO compliance and BAS reporting, while maintaining accrual records for internal management reporting and investor presentations. Modern software like Xero, MYOB and QuickBooks supports this by allowing you to switch report views. However,

your official method declared to the ATO must be applied consistently for tax purposes.

These options make it simpler to prepare accounts and give flexibility to select the method that suits how the business operates.

Accounting Methods Cash vs Accrual: Advantages and Disadvantages

Cash Accounting Benefits

| Advantage | Description |

|---|---|

| Simplicity | Easy to understand and implement |

| Cash Flow Focus | Clear picture of available funds |

| Lower Costs | Minimal bookkeeping requirements |

| Flexibility for Small Operations | Helpful for freelancers and sole traders with simple transactions |

Cash Accounting Limitations

| Disadvantage | Description |

|---|---|

| Limited Insight | Doesn’t show complete business picture |

| Growth Challenges | Less suitable for expanding businesses |

| Loan Difficulties | Banks prefer accrual accounts |

| Planning Issues | Harder to forecast future performance |

| May Delay Income Recognition | Income recorded only when received, skewing short-term results |

| Not GAAP Compliant | Generally doesn’t comply with formal accounting standards |

Accrual Accounting Benefits

| Advantage | Description |

|---|---|

| Complete Picture | Shows true business performance |

| Better Planning | Enables accurate forecasting |

| Professional Image | More credible with stakeholders |

| Growth Ready | Suitable for expanding businesses |

| Compliance with Standards | Meets GAAP/IFRS requirements |

| Improved Cash Management | Tracks receivables and payables for pending cash flow |

Accrual Accounting Limitations

| Disadvantage | Description |

|---|---|

| Complexity | Requires more detailed record-keeping |

| Higher Costs | More expensive to maintain |

| Professional Help | Often requires accountant support |

| Requires Skilled Management | Needs knowledgeable personnel or accountants |

| More Time-Consuming | Increased administrative work can delay reporting |

Switching Between Methods

Can You Change Accounting Methods?

Yes, businesses can switch between cash or accrual accounting methods. However, this requires careful planning and HMRC notification to the relevant regulatory authority.

Switching considerations:

- Tax implications of the change

- Timing of the switch

- Professional advice recommended

- Record-keeping adjustments needed

Accrual Versus Cash Basis of Accounting: Making the Switch

Changes came into force on 6 April 2024, the beginning of the 2024/25 accounting period.

The process involves:

- Deciding on the optimal timing for the change

- Calculating any transitional adjustments needed

- Updating accounting and record-keeping systems

- Notifying HMRC of the change

Practical Implementation of Cash vs. Accruals Accounting

Setting Up Cash Accounting

For cash basis accounting, the requirements include:

- Simple income and expense tracking

- Bank statement reconciliation

- Receipt and invoice filing

- Basic spreadsheet or bookkeeping and accounting software

Setting Up Accrual Accounting

Accrual basis assumption requires more sophisticated systems:

- Accounts receivable tracking

- Accounts payable management

- Prepayment and accrual calculations

- Professional accounting and bookkeeping software

Note: Cash basis accounting records transactions only when cash is received or paid, unlike accrual accounting which tracks transactions when they are incurred regardless of cash flow.

Software to Implement in Cash vs Accrual Accounting

Cash Accounting Software

Popular options include:

- Sage Business Cloud Accounting

- QuickBooks Online Simple Start

- FreeAgent (cash basis mode)

- Xero Starter (simplified features)

Accrual Accounting Software

Comprehensive solutions include:

- Sage Business Cloud Enterprise

- QuickBooks Online Advanced

- Xero Premium

- KashFlow Professional

Record-Keeping Requirements

Cash Basis Records

Accurate and detailed record-keeping is important in cash basis accounting, even though it seems simple.

Maintain:

- All income receipts

- Expense payments and receipts

- Bank statements

- Petty cash records

Accrual Basis Records

Additional requirements include:

- Outstanding invoice lists

- Unpaid bill schedules

- Accrual and prepayment calculations

- Month-end adjustment records

Best Accounting Methods for Australian Businesses

While this guide focuses on Aus rules, similar principles apply globally. The choice between methods depends on:

- Business size and complexity

- Regulatory requirements

- Industry standards

- Growth objectives

Professional Advice and Support

When to Seek Help

Consider professional assistance when:

- Starting a new business

- Switching accounting methods

- Facing complex transactions

- Preparing for growth or investment

Types of Professional Support

Available help includes:

- Qualified accountants

- Bookkeeping services

- Business consultants

- A qualified Xero bookkeeper or financial software specialist who can assist with implementing and optimising your accounting system, especially when transitioning to or managing accrual accounting in Xero.

Professional support like Outsourcing accounting and bookkeeping services can help businesses improve financial reporting accuracy and support strategic decision-making beyond critical transition points.

Future-Proofing Your Choice

Planning for Growth

Consider future needs when choosing between accrual accounting vs cash accounting:

- Anticipated turnover growth

- Potential investors or lenders

- Business structure changes

- Market expansion plans

Regular Reviews

Assess your accounting method annually:

- Business performance changes

- New regulatory requirements

- Technology improvements

- Cost-benefit analysis

Accrual Accounting vs Cash Accounting for Businesses: Decision Framework

Use this framework to choose the right method:

Step 1: Assess Current Situation

- Calculate annual turnover

- Evaluate business complexity

- Consider cash flow patterns

- Review regulatory requirements

Step 2: Consider Future Plans

- Growth projections

- Investment needs

- Market expansion

- Structure changes

Step 3: Evaluate Resources

- Available time for bookkeeping

- Professional support budget

- Technology capabilities

- Staff expertise

Step 4: Make Informed Decision

- Compare method benefits

- Calculate implementation costs

- Plan transition if needed

- Set review schedule

Common Mistakes to Avoid

Cash Accounting Pitfalls

- Ignoring unpaid invoices in planning

- Mixing personal and business transactions

- Poor record-keeping despite simplicity

Accrual Accounting Errors

- Inconsistent cut-off procedures

- Missing accrual calculations

- Inadequate supporting documentation

- Complex adjustments without help

Compliance and Audit Considerations

HMRC Requirements

Both methods must comply with:

- Accurate record maintenance

- Timely tax return filing

- Supporting documentation

- Consistent application

Audit Readiness

Maintain audit trails through:

- Complete transaction records

- Regular reconciliations

- Document retention policies

- Professional review processes

Technology and Automation

Modern Accounting Solutions

Today’s software offers:

- Automatic bank feeds

- Receipt scanning capabilities

- Real-time reporting

- Cloud-based accessibility

Integration Benefits

Connected systems provide:

- Reduced manual entry

- Improved accuracy

- Time savings

- Better insights

Conclusion

The choice between accrual accounting vs cash accounting significantly impacts your business operations. Cash accounting offers simplicity but limited insight.

Accrual accounting provides comprehensive financial pictures but requires more effort. Consider your business size, complexity and future plans.

From April 2024, HMRC will presume that a business is using cash basis accounting unless the owner makes an election to use accruals basis. This change emphasises the importance of making an informed choice.

For 2025, remember that businesses with a turnover above $10 million must use accrual accounting for GST and financial reporting, while those below this threshold can continue using cash accounting if it suits their operations. Always ensure your records and reporting align with the latest ATO requirements for the current financial year.

Regular reviews ensure your chosen method continues serving your business needs. Professional advice helps navigate complex decisions and changes.

Frequently Asked Questions

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.