Most business owners think AI in accounting is mainly about faster data entry. While that is certainly one benefit, the bigger change is the insight it provides. AI helps accountants identify patterns in cash flow, detect unusual expenses and spot gaps in reporting that could otherwise take days to uncover, if they are noticed at all.

For Australian businesses, that shift has a direct implication. The accounting support you are paying for should now be giving you more than accurate numbers. It should be giving you clearer, faster insight into what those numbers mean for your business.

This guide covers what AI actually does inside an accounting workflow, where professional judgement still has to be involved and how to tell whether your current setup is making proper use of it. The gap between what AI promises and what it delivers in practice is wider than most software vendors suggest.

Key takeaways

- AI gives your accountant real-time visibility into cash flow patterns, expense anomalies and reporting gaps not just faster data entry.

- Only 15% of Australian small businesses invested heavily in AI in 2025 half the Asia-Pacific average.

- AI handles volume well. It does not handle complex judgement calls or unusual situations that require business-specific knowledge.

- Faster reports and fewer manual requests are signs AI is working.

- Outsourcing accounting services to an AI-enabled accounting firm gives small businesses access to capability they could not build in-house.

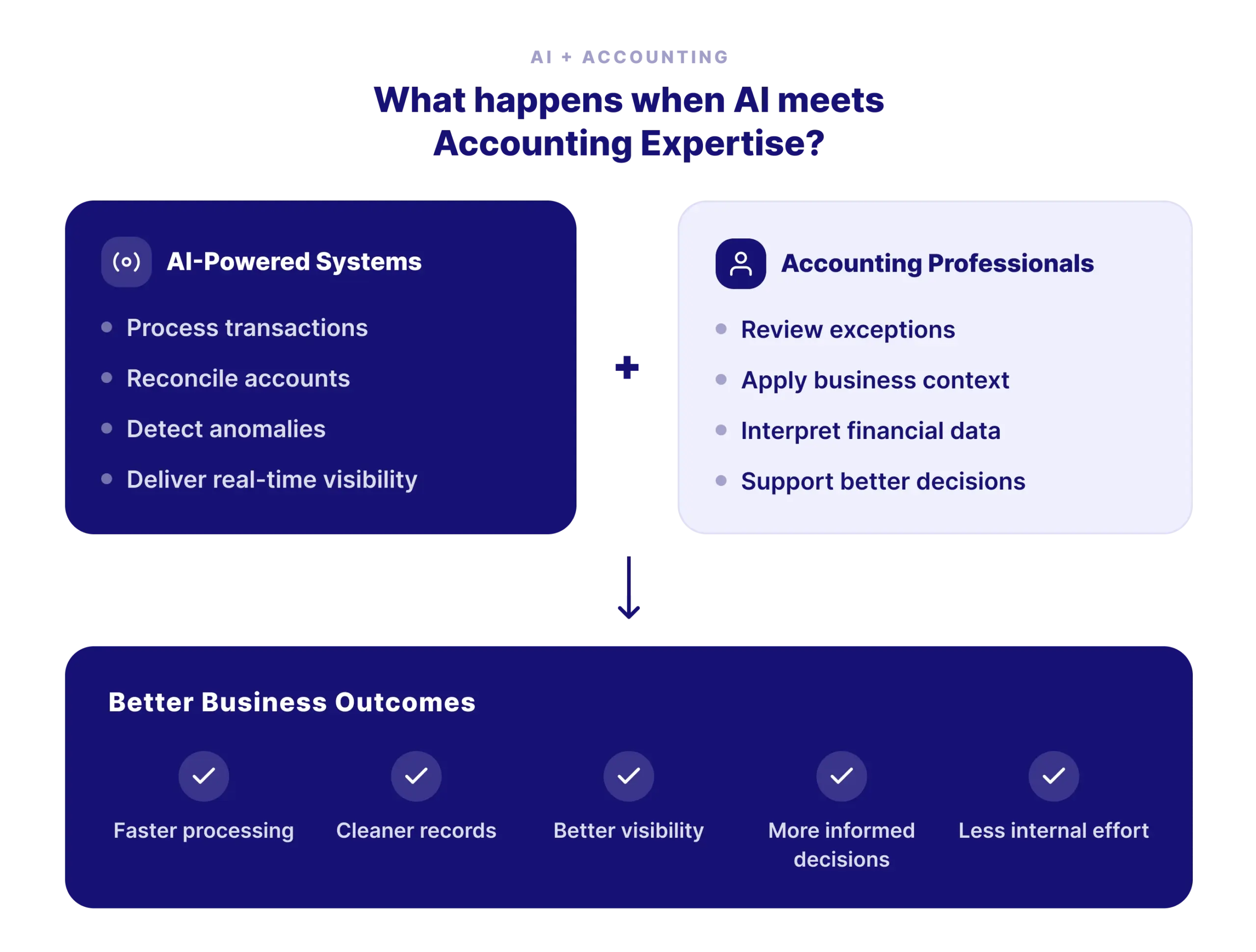

What AI actually does inside an Accounting Workflow?

AI does not replace the accounting process. It changes how much of that process requires a human to sit down and do it manually.

For a business owner, that distinction matters because it determines how quickly your numbers are ready, how accurate they are and how much of your accountant’s time goes toward checking data versus interpreting it.

Data entry and invoice processing

Every invoice your business receives needs to be read, checked and recorded. Manually, that means someone opening each document, pulling out the relevant details and entering them into the system.

AI does this automatically. It reads the invoice, extracts the vendor name, amount, date and line items and codes it to the right account. What used to take hours across a week of transactions now happens as the invoices come in.

Bank reconciliation

Matching transactions in your bank statement to entries in your accounting records is one of the most time-consuming parts of any month-end process.

AI handles this by pulling live bank data and matching it to recorded transactions automatically. Discrepancies get flagged for review. Clean matches get cleared. Your accountant spends time on the exceptions, not the entire list.

Anomaly detection

This is where AI moves beyond speed and into something more useful. As it processes your financial data, it learns what normal looks like for your business your typical expense patterns, your usual vendor amounts, your regular payment cycles.

When something falls outside that pattern, it flags it. A duplicate payment, an unusual vendor charge, a transaction posted at an odd time these are the things that slip through in manual review. Businesses that want to avoid mistakes in their financial records benefit most from this layer of automated detection.

Reporting and cash flow visibility

Once your data is clean and current, reporting becomes faster and more useful. Instead of waiting for a manual month-end close to see how your business is performing, AI-enabled accounting can give you an up-to-date picture at any point in the month.

Cash flow positions, expense trends and revenue patterns are visible in close to real time rather than weeks after the fact.

Where Human Judgement still has to be involved?

AI is good at processing what it can see and measure. Where it falls short is in situations that require professional judgement unusual transactions, strategic decisions and anything where the numbers alone do not tell the full story.

That difference is important for any business owner to understand, because it defines exactly where your accountant’s expertise still matters and why no amount of automation replaces the need for a thinking person reviewing your finances.

Expense Classification requires Human Judgment

AI classifies transactions using keywords and past patterns. That works for routine expenses, but some transactions require context and judgment.

For example, a business trip may include a dinner expense. Whether it is recorded as client entertainment or staff subsistence depends on who attended, the purpose of the meal and the business’s own policies. AI may classify it based on the word “dinner,” while an accountant considers the full context before making the decision.

The same applies when a business uses custom expense categories or has specific recording preferences. An accountant understands those requirements and applies them consistently, while AI can only follow the rules it has been given.

Unusual or one-off transactions

Most AI systems learn from patterns. When a transaction breaks that pattern without explanation, AI can identify it but cannot interpret it. A one-off asset purchase, an irregular intercompany transfer or a settlement payment all look suspicious to an algorithm.

Your accountant knows the story behind the number. That context is what turns an unresolved entry into a correctly recorded one.

For example, a construction business that pays a large lump sum to a new supplier mid-year will likely be marked for review. To AI, it looks unusual.

To the accountant who knows that business just started a new project requiring upfront materials, it is completely expected. Without that conversation, the entry either gets misclassified or sits unresolved.

Handling incomplete or poor-quality data

AI performs best when the data it receives is complete and accurate. If an invoice is blurry or important information is missing, it may fail to read the document correctly or simply flag an error.

An accountant takes the next step. They can identify what is missing, request the required information and use their understanding of the client’s records to resolve issues accurately.

Commercial and strategic decisions

AI can identify trends and highlight unusual changes in financial data. Understanding what those changes actually mean is a different matter.

For example, higher spending during a busy season could reflect increased demand, planned growth or rising cost. An accountant evaluates those figures in the context of how the business operates before drawing conclusions.

The same applies to strategic decisions. Questions such as whether to take a salary or dividends involve business goals, financial planning and other important considerations. AI can present the numbers, but an accountant provides the judgment needed to make the right decision.

Client relationships and advisory conversations

AI can analyse financial data and highlight trends, but it cannot replace the conversations that help business owners make important decisions.

For example, a business may show strong revenue growth alongside declining profit margins. AI can identify both trends, but it cannot determine whether the business should expand, reduce costs, or delay investment. Those decisions require professional judgment, business context, and an understanding of the owner’s goals.

AI provides the information. Accountants provide the advice that turns those insights into informed business decisions.

When an anomaly needs a decision

AI is effective at analysing large volumes of financial data and flagging unusual transactions or patterns. However, identifying an issue is only the beginning. Someone still needs to decide the appropriate response.

- AI highlights anomalies but cannot determine the right course of action.

- Accountants investigate the issue, validate the data and decide whether adjustments or escalation are required.

- Human judgement provides the business context needed to interpret financial information accurately.

- AI improves speed and efficiency, while people ensure accuracy, accountability and informed decision-making.

The greatest value comes from combining AI with human expertise. While AI identifies what needs attention, accountants ensure the right decisions are made.

Where AI still needs Human Expertise?

AI can automate routine accounting tasks, but it still struggles when work requires judgment, context, or interpretation. Some common examples include:

- Interpreting complex rules: AI can apply standard rules, but unusual transactions or industry-specific requirements often need professional judgment.

- Handling exceptions: Blurry invoices, missing information, duplicate transactions, or reconciliation issues usually require human review.

- Reconciling complex payments: Part payments, overpayments, bulk payments, and intercompany transactions cannot always be matched accurately without oversight.

- Managing payroll changes: Payroll adjustments and changes to statutory rules need careful interpretation before they are applied.

- Interpreting financial reports: AI can generate reports, but accountants explain what the numbers mean and how they affect business decisions.

- Resolving data and system issues: When accounting software or integrations produce incorrect data, accountants identify the cause, correct the records, and resolve the issue.

- Verifying AI outputs: AI can occasionally produce incorrect results or inaccurate insights. Human review is essential before financial information is used for reporting or decision-making.

How Australian Businesses are Actually Using AI in 2026?

Understanding what AI can do is one thing. Deciding how to use it effectively is another.

Australian businesses are adopting AI at different rates. While some are investing in dedicated AI tools, others are using AI capabilities already built into their accounting software. Many are still evaluating where AI fits within their operations.

AI adoption is happening in everyday work:

Even without formal AI strategies, business owners, accountants and finance teams are using tools such as ChatGPT, Google Gemini and Microsoft Copilot to:

- Draft client emails

- Summarise financial reports

- Prepare advisory meeting notes

- Reduce time spent on administrative tasks

What the research says:

- CPA Australia’s Australian small business AI adoption and productivity data from April 2026 found that only 15% of Australian small businesses invested heavily in AI in 2025, against a 32% Asia-Pacific average. Only 30% said that investment improved profitability one of the lowest results across the region.

- The Reserve Bank of Australia’s November 2025 review of technology investment across Australian firms added further context. Across surveyed firms, adoption of AI tools has been largely employee-led rather than employer-led, with returns described as mixed and expected to take time to be realised.

How businesses are accessing AI in Accounting:

- Managing AI internally: Purchase AI-enabled bookkeeping software, build workflows and train staff. This provides greater control but requires ongoing time, expertise and investment.

- Using AI within existing accounting software: Many businesses already have access to AI-powered features such as bank reconciliation, invoice capture and cash flow reporting through platforms like Xero, MYOB and QuickBooks.

- Working with an outsourced accounting provider: Businesses gain the benefits of AI-enabled processes and experienced professionals without managing the technology themselves.

As AI adoption continues to grow, businesses are choosing the approach that best matches their resources, internal capabilities and long-term goals.

AI Accounting Tools used in Practice

Understanding how AI is used in accounting is only the first step. The real value comes from knowing which tools support day-to-day accounting tasks and how they fit into existing workflows.

Choosing the right approach depends on the needs of the business, the level of internal resources available, and how quickly the business wants to see results

- Xero: Automated bank reconciliation, invoice capture and real-time cash flow dashboard. Businesses exploring this platform can review Xero pricing to understand which plan suits their needs.

- MYOB: Automated transaction matching, payroll processing and financial reporting.

- QuickBooks: Smart transaction categorisation, anomaly alerts and cash flow forecasting.

- Xbert.io: An AI-powered audit and anomaly detection layer that sits on top of Xero, flagging issues before they become errors.

- Hubdoc and Dext: document capture tools that extract data from receipts and invoices and auto-code them to the correct accounts, functioning as automated bookkeeping software within a cloud accounting setup.

AI and Outsourcing: Better Together

AI has changed how accounting work is completed, but it has not removed the need for outsourcing accounting. The greatest value comes from combining AI with experienced accounting professionals.

The most effective accounting setups today are not built on AI alone or on people alone. They are built on both working together, each handling what it does best.

For Australian businesses, this combination is already accessible. The question is whether the accounting firm or provider they work with has actually built it into how they operate.

What AI does well:

- Extracts data from invoices and receipts

- Automates transaction coding and allocation

- Processes recurring journal entries

- Generates standard financial reports

- Identifies patterns, trends, and anomalies in financial data

What experienced accountants do that AI cannot:

- Handle complicated transactions and interpret what they mean

- Apply contextual judgement to decisions

- Maintain quality control and compliance

- Manage complex client relationships

- Correct errors that AI does not recognise as errors

Why they work better together

- AI automates repetitive, high-volume tasks, allowing accountants to focus on higher-value work.

- Automation improves speed and consistency, while human review maintains accuracy and quality.

- Accountants verify AI-generated outputs, resolve exceptions, and ensure financial information can be relied upon.

- Businesses benefit from greater efficiency without compromising professional oversight.

For Australian businesses, the question is no longer whether to choose AI or outsourced accounting. The real value comes from using both together, with AI improving efficiency and accountants providing the expertise, judgment, and oversight that technology cannot replace.

What AI-enabled Outsourcing Accounting looks like today?

In practice, many accounting firms combine automation with professional oversight, allowing businesses to benefit from both technology and human expertise without managing AI internally.

Businesses working with AI-enabled accounting providers can typically expect:

- Faster processing of invoices and routine transactions.

- Automated reconciliations and identification of unusual activity.

- Financial information that is more current and easier to review.

- Accountants who investigate exceptions, apply business knowledge and help interpret results.

- Reduced administrative effort associated with selecting software, training staff and maintaining AI workflows.

For many small businesses, outsourcing accounting services provides a practical way to access capabilities that may be difficult or expensive to build in-house.

Looking for hands-on, AI-enabled bookkeeping support? Meet our Brisbane accounting team who combine smart automation with local expertise.

Is AI actually improving your Accounting?

AI being present in your accounting process does not automatically mean it is working well for your business. The tools matter less than the outcomes they produce. These are the signs worth paying attention to.

Signs AI may be improving your accounting include:

- Reports are available sooner and reflect more current information.

- Transactions are categorised consistently with fewer manual corrections.

- Repeated requests for the same documents become less frequent.

- Unusual transactions are identified and discussed proactively.

- Accountants spend more time explaining results and less time chasing paperwork.

Signs it may not be delivering value include:

- Month-end reporting still takes weeks to complete.

- Financial information regularly needs to be reworked manually.

- Processes look largely the same despite claims of AI adoption.

- Most interactions still focus on gathering information rather than discussing what it means for the business.

Questions worth asking your provider:

- Which parts of the process are automated?

- How are exceptions identified and resolved?

- How quickly are records updated after a transaction occurs?

A provider using AI effectively will answer these specifically. Vague responses about technology and efficiency are not the same as a clear explanation of how the work actually gets done.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

The impact of AI in accounting is not determined by whether a business uses AI tools. It depends on whether those tools improve the quality, timeliness and usefulness of financial information.

For some businesses, investing in software and building internal workflows makes sense. For others, accessing AI-enabled accounting through an outsourcing provider or working with a certified Xero bookkeeper to configure existing tools correctly offers a practical way to benefit from automation and cleaner records without managing the technology internally.

Outbooks provides AI-enabled outsourcing accounting services to Australian businesses. Call 0451 320 102, email info@outbooks.com.au to discuss your requirements.

FAQs

Parul is a content specialist with expertise in accounting industry. Her writing covers a wide range of domains such as, Accounts Payable, Accounts Receivables, Bookkeeping and more. She writes well-researched content and has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.